Environment

Environment Economic

Economic Social

Social

Environment

Environment12 Consecutive years

15 years in a row

for the last 10 years

This Initiative reaches out to over 6.4 million citizens

Over 48% of ITC's Total Energy Requirements met from carbon neutral sources.

22 green buildings

Economic

EconomicTurnover has grown 11-fold

Profit has grown 39 times

Total Shareholder Returns has grown at a CAGR of 23.6%

Over $50 billion

Over $8 billion

Social

SocialEmpowering 4 million farmers

Generating over 110 million person-days of employment

Covering nearly 55,000 rural women

Benefitting over 5,25,000 children

Services provided to over 15,00,000 milch animals

Covering nearly 12,500 acres

Training over 46,000 youth

Over 25,000 low-cost sanitary units constructed

It has been our resolve to build an exemplary Indian enterprise that would create enduring value for our country. An organisation that would adopt the credo of putting 'India First' - keeping Country before Corporation and the Institution before the Individual. Over the years, the patriotic sense of 'India First' has grown into a full-blown aspiration to be a National Champion subserving the country's larger priorities. This is not only manifest in the creation of world-class Indian brands, but also in the Triple Bottom Line goals of the Company to nurture larger societal value. The need to sustain global competitiveness in economic value creation, whilst simultaneously creating larger societal value, has led to innovation in business models that seek to synergise the building of economic, ecological and social capital as a unified strategy.

A new paradigm of growth is today called for - an integrated Triple Bottom Line approach that builds competitiveness whilst at the same time ensuring that the environment is nourished and large-scale sustainable livelihoods are created. I call this new paradigm 'Responsible Competitiveness', which to my mind is a pre-requisite to creating a more sustainable future.

'Enterprises of Tomorrow' can bring in transformational change by making societal value creation a conscious strategic decision and not one that banks on corporate conscience alone. ITC has always believed that businesses possess unique strengths to make a larger contribution to society. If the creative and innovative energies that businesses employ to create world-class products and brands are leveraged to deliver social initiatives that serve a larger national objective, it can have a transformative impact on society.

It is this belief that has spurred ITC to craft innovative strategies that orchestrate a symphony of efforts aimed at enriching the environment, creating sustainable livelihoods, empowering local communities and addressing the challenge of climate change.

The global economy remained on a decelerating trend in 2016 growing by 3.1% compared to 3.4% in 2015 (as per latest IMF estimates). This marks the slowest pace of expansion since the global financial crisis Snapshot of Economic Performance in 2009 and the 5th successive year that the global economy has grown at a rate lower than its long-term average of 3.6% p.a. The anticipated pickup in global growth (3.4%) at the beginning of the year did not fructify mainly due to slower growth in the Advanced Economies which grew by 1.7% in 2016 against 2.1% in 2015. Within the Advanced Economies, the US posted a muted growth of 1.6% led by downward adjustments in inventories and contraction in Private Investments, particularly during the first half of the year. The Euro Area also recorded tepid growth, expanding by 1.7% during the year compared to 2.0% in 2015. Emerging Market & Developing Economies witnessed a growth of 4.1% in 2016 against 4.2% in 2015, with Brazil and Russia recording a reduced pace of contraction which was offset by slower growth in the emerging European economies and further slowdown in the Chinese economy from 6.9% in 2015 to 6.7% in 2016.

In spite of the lacklustre performance during the year as aforestated, green shoots of economic recovery became visible in the latter half of the year. It is anticipated that the global economy will perform better and grow by 3.4% in 2017 and improve further to 3.6% in 2018, on the back of synchronised growth momentum in Advanced as well as Emerging Economies. After years of persistently low inflation (even deflation), 2017 is expected to be a year of reflation. Stronger growth momentum, better prospects for oil and other commodities, and the US Dollar's appreciation against other major currencies could cause inflation to return in most major economies.

The Indian economy witnessed another challenging year, with Real GDP growth pegged at 7.1% representing a sharp slowdown over 2015-16 (7.9%). Further, looking beyond the reported numbers, a wide range of economic indicators suggest tepid performance across private investments, consumption and manufacturing activity which have contracted significantly. The anticipated pickup in consumption and private investments remained elusive.

Private Investments are estimated to have grown by a mere 0.6% in 2016-17 a 5-year low. Indian industry continues to be adversely impacted by low capacity utilisation and stretched balance sheets. Growth in Private Final Consumption Expenditure (PFCE) is estimated at 7.2% for 2016-17 (compared to 7.3% in 2015-16) aided by a rebound in Agriculture on the back of a good monsoon after two consecutive years of sub-par rainfall, partial implementation of recommendations of 7th Pay Commission and 'One Rank One Pension' (OROP) scheme. However, proxy indicators such as subdued performance of two-wheeler sales, weak power demand, decline in cement and oil volumes and a marked deceleration in corporate sales growth, point to persistent weakness in Private Consumption.

The performance of the Industry sector also remained muted as reflected by the Index of Industrial Production (IIP) which grew by just 0.4% during the period April 2016 to February 2017 as against 2.6% in the same period last year. Further, IIP (Manufacturing sector) witnessed a de-growth of 0.3% during the period April 2016 to February 2017 (compared to growth of 2.3% in the same period last year).

On the positive side, India remains the fastest growing major economy in the world. During the year, there was significant improvement on the 'twin deficit' front. Fiscal Deficit is estimated to be contained within target at 3.5% of GDP in 2016-17 (against 3.9% in 2015-16) aided by buoyant tax collections and decline in oil subsidies. The Current Account Deficit was also contained within 1.0% of GDP in spite of an increase in oil prices during the year.

Inflation remained largely within the comfort zone of the RBI during the year. Wholesale Price Index (WPI) for 2016-17 increased to 3.7% from (-) 2.5% in 2015-16, which was mainly attributable to the base effect of low fuel and commodity prices. Consumer Price Index (CPI) for 2016-17 declined to 4.5% against 4.9% in 2015-16 with Core CPI remaining stable at 4.7% in 2016-17 (4.6% in 2015-16). This prompted the RBI to reduce policy interest rates by 50 bps during the year.

Driven by the foreign capital flow into the country, in the form of Foreign Institutional Investments and Foreign Direct Investment, Sensex advanced 17% (after declining by 9% in 2015-16), reflecting the optimism on improvement in the business environment, expected progress on the reforms agenda and anticipated acceleration in future corporate earnings. The pace of growth is expected to gather momentum in the medium term on the back of favourable global economic tailwinds, implementation of key policy reforms such as Goods and Services Tax (GST) and pickup in private investment.

Given the macro-economic scenario, the Company delivered a steady performance during the year in the backdrop of a persistently sluggish demand environment, continuing pressure on the legal cigarette industry due to the cumulative impact of steep increase in taxation and regulatory pressures, sharp hike in input costs and gestation costs relating to new products/ categories especially in the non-cigarette FMCG segment. The operating environment was rendered particularly challenging in the second half of the year with the currency crunch impacting the incipient recovery in demand. The business environment in the Hotels industry also remained subdued, with only a marginal improvement in room rates reflecting the overhang of excess room inventory in key markets. The Paperboards, Paper and Packaging segment also had to contend with a weak demand and pricing environment.

Despite the challenging business environment as aforestated, Gross Revenue from sale of products and services stood at 55001.69 crores and grew by 6.6% primarily driven by an 8.0% growth in the non-cigarette FMCG segment, 10.8% growth in Agri Business and 5.1% growth in the Cigarettes segment. Profit Before Tax registered a growth of 7.4% to 15502.96 crores while Profit After Tax at 10200.90 crores increased by 9.4%. Total Comprehensive Income for the year stood at 10277.90 crores (previous year 9261.79 crores). Earnings Per Share for the year stood at 8.43 per share (previous year 7.74 per share). Cash flows from Operations aggregated 15214.98 crores, compared to 14039.64 crores in the previous year.

For the year ended March 31, 2017, the Board of Directors have recommended an Ordinary Dividend of 4.75 per share (previous year Ordinary Dividend of 4.33 per share and Special Dividend of 1.33 per share; adjusted for Bonus Issue). Total cash outflow in this regard will be 6944.65 crores including Dividend Distribution Tax of 1174.64 crores.

Despite the extremely challenging business environment during the year under review, ITC continued to make significant investments in the Indian economy across its business domains. This included investments in manufacturing facilities towards sustaining its competitive advantage, which included state-of-the-art, on-line quality oversight systems and cutting-edge technology for innovative packaging.

Apart from the above, Company continued to invest towards enhancing brand salience and consumer connect, while simultaneously implementing strategic cost management measures across the value chain. Several initiatives were also implemented during the year towards leveraging the rapidly growing e-commerce channel with a view to enhancing the reach of the Company's products and harnessing digital and social media platforms for deeper consumer engagement. Substantial investments are also being made in Research & Development with focus on consumer insight discovery to develop and launch disruptive and breakthrough products in the market place.

ITC's diversified portfolio of businesses, spanning FMCG, Paperboards & Packaging, Agri Business and Hotels enables it to have significant presence in all the three sectors of the economy, namely, agriculture, manufacturing and services, providing the Company the unique opportunity to contribute meaningfully to the growth and development of the country.

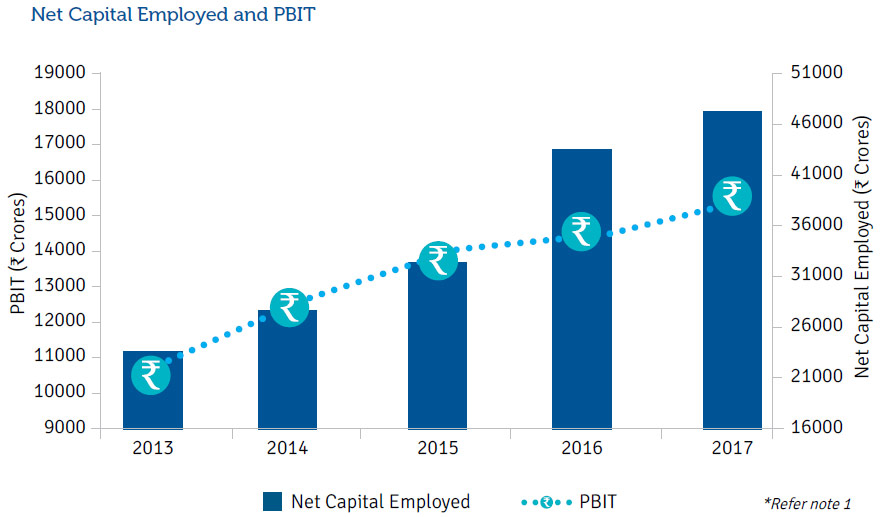

Hence, while the net capital employed* has expanded at a compound rate of 14% over the previous five years to reach 40,278 crores as on March 31, 2017, returns on net capital employed (Profit before interest and taxes) have increased during this period from 17,160 crores to 23,810 crores, a compound rate of 9%.

ITC is one of India's most admired and valuable corporations and has consistently featured over the last twenty years, amongst the top 10 private sector companies in terms of market capitalisation and profits. Over the last 21 years, the Company has created multiple drivers of growth by developing a portfolio of world-class businesses across all sectors of the national economy spanning agriculture, manufacturing and services; placing the Company amongst the foremost in the country in terms of efficiency of servicing financial capital.

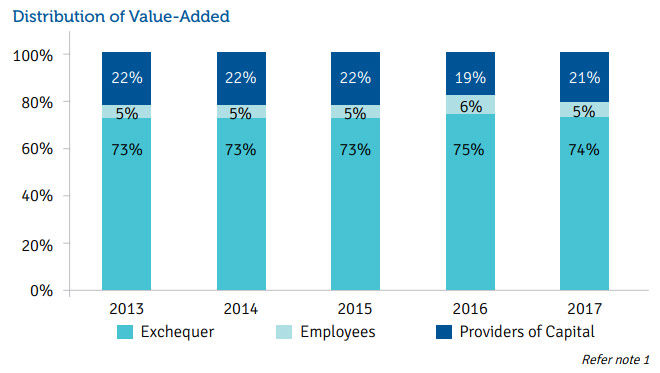

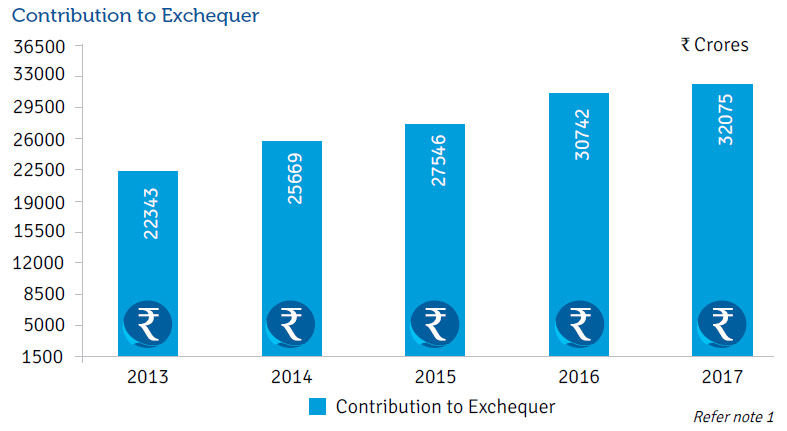

The Value-Added by the Company, i.e. the value created by the economic activities of the Company and its employees, grew by 6% over last year to 43,568 crores. The Company's Contribution to Exchequer during the year stood at 32,075 crores representing 74% of the total value addition made by the Company.

The Company remains amongst the Top 3 Indian corporates in the private sector in terms of Contribution to Exchequer.

For the year ended March 31, 2017, the Board of Directors have recommended an Ordinary Dividend of 4.75 per share (previous year Ordinary Dividend of 4.33 per share and Special Dividend of 1.33 per share; adjusted for Bonus Issue).

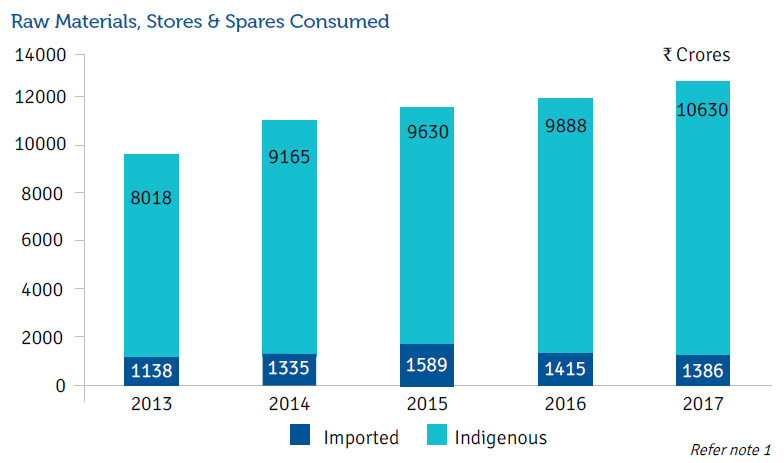

The Hon'ble Prime Minister's vision to build a dynamic, progressive and self-reliant India through impactful programmes such as the Make in India, Skill India, Digital India and Swachh Bharat resonates deeply with the Company's efforts to create a national institution of pride. The Company actively encourages competency development among local vendors and its vendor base including numerous medium and small scale enterprises that are proximate to its manufacturing locations. More than 87% of raw materials and stores & spares have been locally procured during the year.

The Company's suppliers, both local and international, constitute one of its important stakeholder groups. Vendors/service providers and large outsourced manufacturing facilities are encouraged to adopt management practices detailed under the international standards such as ISO 9001, ISO 14001, OHSAS 18001 and ITC's Corporate Environment, Health and Safety (EHS) Guidelines. In order to strengthen sustainable procurement processes, Policies on 'Responsible Sourcing' and 'Human Rights Consideration of Stakeholders beyond the Workplace' have been adopted to address issues of labour practices, human rights, bribery, corruption, occupational health, safety and environment. Please refer to 'Business Responsibility Report' of the Report and Accounts 2017 (available on www.itcportal.com) for discussion on sustainability of products and services across life-cycle, supply chain and product responsibility etc.

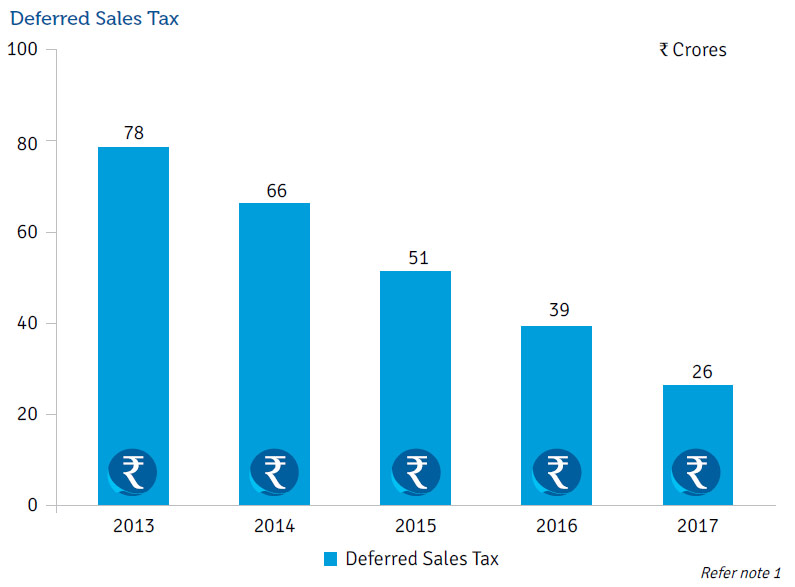

The Company had availed the incentives offered by the States of Andhra Pradesh and Tamil Nadu, by way of deferment of Sales Tax, which are repayable over a period ranging from 10 to 14 years. The outstanding amount of such assistance in the form of Deferred Sales Tax due to be repaid by the Paperboards and Specialty Papers Division (PSPD) is given below:

Other Government grants received in the form of incentives such as Export Promotion Capital Goods, Service Export from India Scheme, Merchandise Export from India Scheme amounted to 127.01 crores (2016 - 71.92 crores).

Human Resource Management systems and processes in the Company are aimed at creating a responsive, market-focused, customer-centric culture and enhancing organisational vitality, so that each business is internationally competitive and equipped to seize emerging market opportunities. The Company believes that the robustness and adaptability of its Human Resource systems and processes are critical for an organisation to remain relevant and competitive in today's highly dynamic and rapidly evolving business landscape.

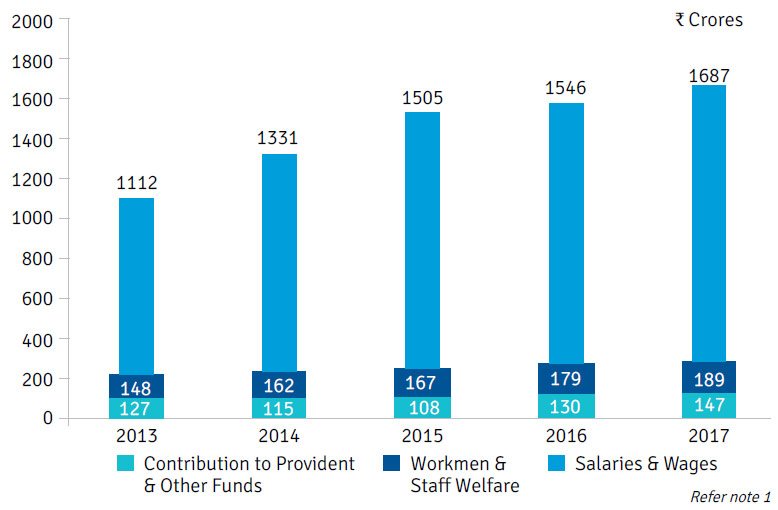

The superior capability of the Company's talent pool is premised on a work culture that nurtures quality talent and promotes a conducive work environment that combines the need to focus on performance and results with a caring and compassionate work ethos. Policies on 'Diversity and Equal Opportunity', 'Freedom of Association' and 'Environment, Health and Safety', among others, guide the management approach on specific elements of the Company's work practices. ITC believes that its competitive capability to build futureready businesses and create enduring value for stakeholders is enriched by a dedicated and high-quality human resource pool. It has continuously invested in the human resource capital as seen below:

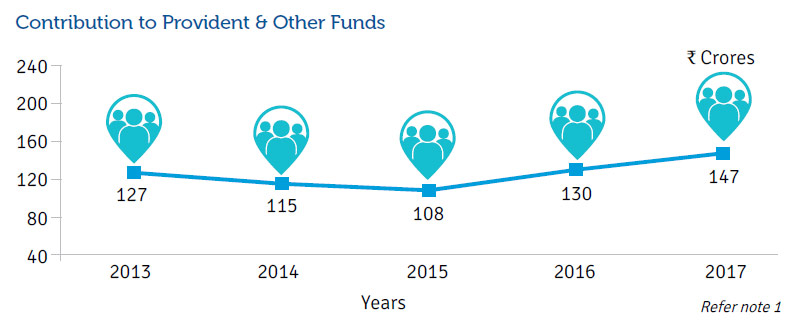

The employees are also entitled to retirement benefit schemes which include employee pension, provident fund and gratuity. All statutory payments, as applicable, e.g., Provident Fund and Family Pension contributions, are deposited with the Government in a timely manner.

The pension plans and other applicable employee benefits obligations are determined and funded in accordance with independent actuarial valuation. The assets of these trust funds are managed in accordance with the prescribed statutory pattern. The assets of the trust funds are well diversified and investments are made with the objective of protecting capital and optimising returns within acceptable risk parameters. The funds are consistently sustained to meet requisite superannuation commitments.

ITC's overarching aspiration to create significant and sustainable societal value is manifest in its CSR initiatives that embrace the most disadvantaged sections of society, especially in rural India, through economic empowerment based on grassroots capacity building. Towards this end, the Company has adopted a comprehensive CSR policy outlining programmes, and plans to undertake projects and activities to create a significant positive impact on identified stakeholders. All these programmes fall within the purview of Schedule VII of the provisions of Section 135 of the Companies Act, 2013 and the Companies (Corporate Social Responsibility Policy) Rules, 2014. The footprint of the Company's Social Investments Programme (SIP) projects is spread over 26 states covering 184 districts.

The key elements of the Company's CSR interventions are to:

The Company's stakeholders are confronted with multi-dimensional and inter-related issues, at the core of which is the challenge of securing sustainable livelihoods. Accordingly, interventions under the Company's Social Investments Programme (SIP) are appropriately designed to build their capacities and promote sustainable livelihoods.

Various CSR activities in which the Company has been engaged during the current year are listed below:

The expenditure incurred under Section 135 of the Companies Act, 2013 on CSR activities amounted to 275.96 crores (2016 - 247.50 crores).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}