In line with ITC's philosophy of creating enduring value for all its stakeholders, ITC has adopted a structured approach to building partnerships in sustainable business practices. ITC's approach to stakeholder engagement is based on the long term stable relationships that it has fostered with key stakeholders such as shareholders, farmers, customers, suppliers, employees, local communities, regulatory bodies, media etc. Recognising that stakeholder engagement is an integral part of partnership building, ITC has endeavoured to institutionalise these existing relationships through a formal process that includes:

- Identification of key stakeholders

- Consultation with the key stakeholders

- Identification and prioritisation of concerns and needs

- Addressing the prioritised concerns and needs in a consistent and transparent manner

ITC identifies and profiles stakeholder groups as well as individual stakeholder representatives who are directly/indirectly impacted by its business activities as well as those who can directly or indirectly exert influence on its business activities. While selecting stakeholder representatives, attempts are made to ensure that they genuinely represent the views of their constituents, and can be relied upon to faithfully communicate the results of the engagements with ITC, back to their constituents.

Stakeholders' identification is guided by the attributes of stakeholders such as:

DEPENDENCY

Groups or individuals who are directly or indirectly dependent on the organisation's activities, products or services and associated performance, or whom the organisation is dependent on for operations e.g. shareholders, employees, farmers, suppliers, service providers and

local communities.

RESPONSIBILITY

Groups or individuals to whom the organisation has, or potentially envisaged to have, legal, commercial, operational or ethical responsibilities e.g. customers; providers of financial capital.

IMMEDIACY

Groups or individuals who need immediate attention from the organisation with regard to economic, social or environmental issues.

INFLUENCE

Groups and individuals who can have impact on the organisation's or a stakeholder's strategic or operational decision-making e.g. Providers of financial capital; Government and Regulatory Authorities.

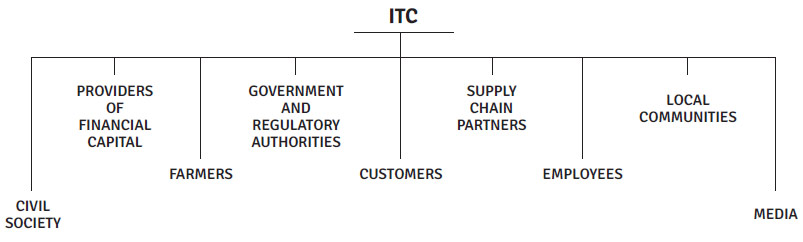

Therefore, broadly the key stakeholders identified by ITC include,

- Providers of financial capital

- Customers

- Employees

- Supply chain members

- Farmers

- Government and Regulatory Authorities

- Local Communities

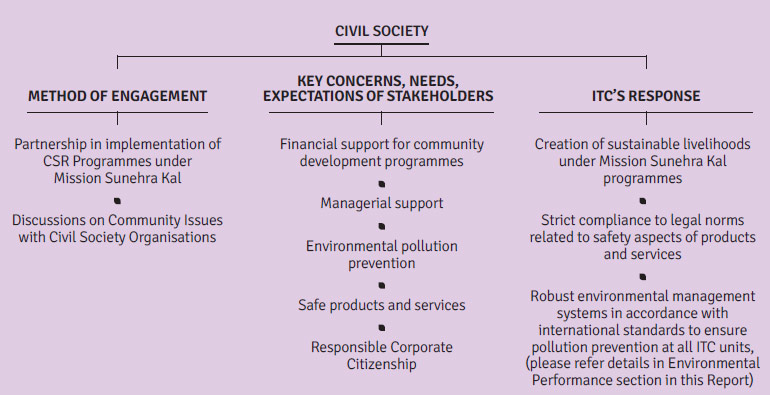

- Civil society

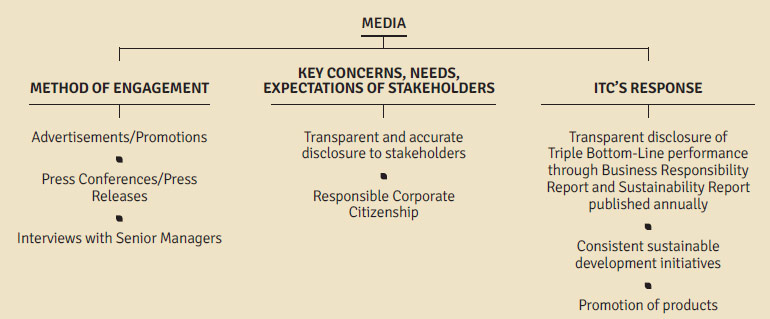

- Media

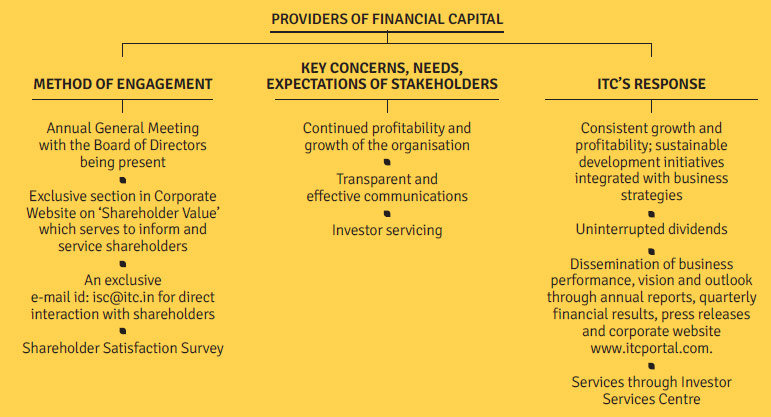

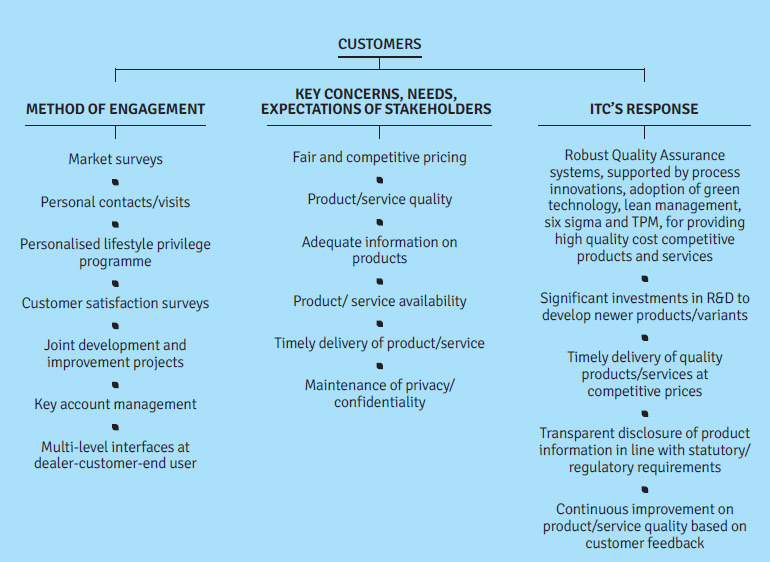

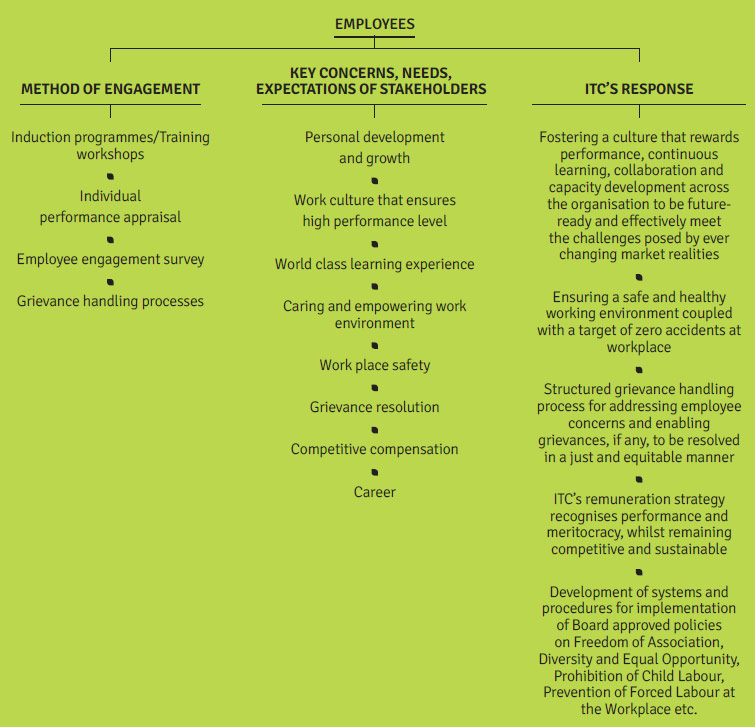

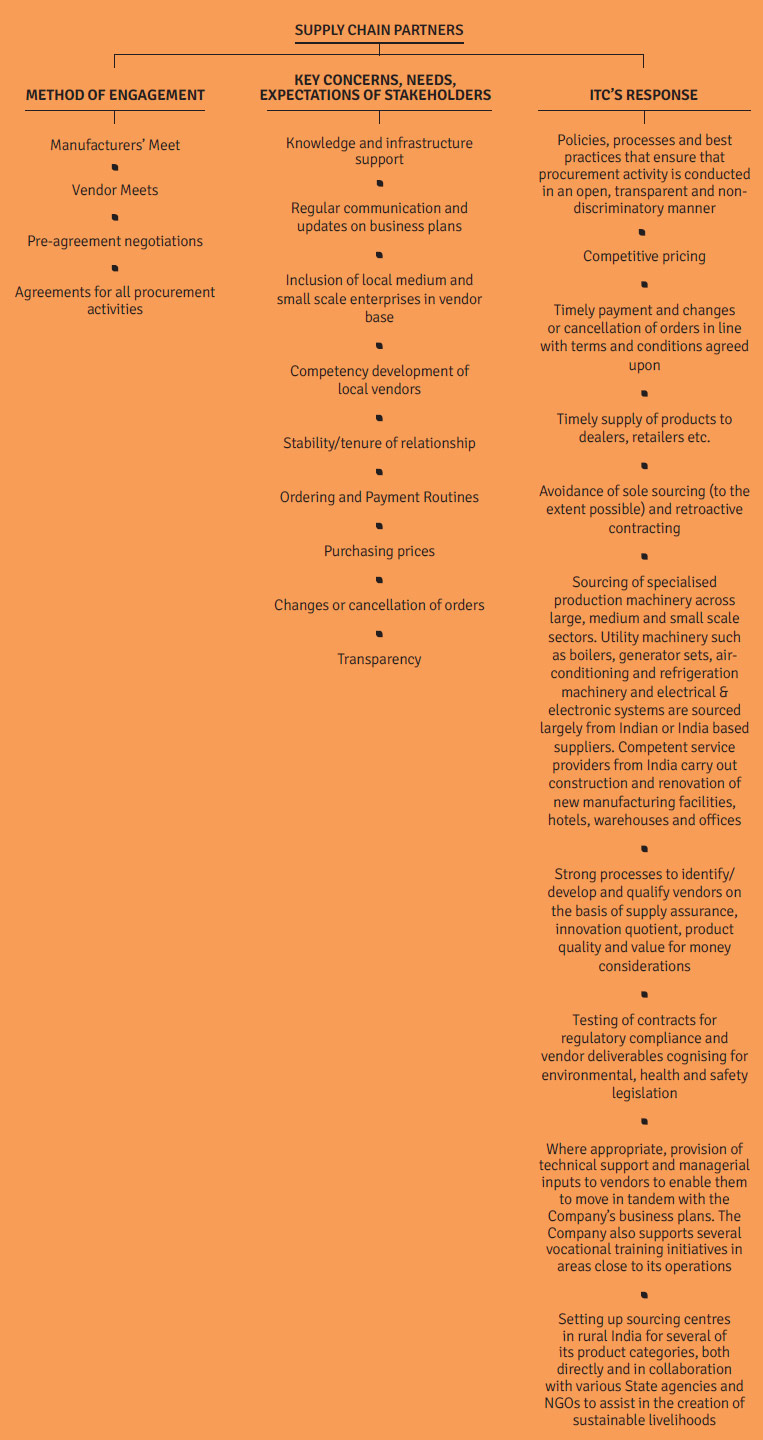

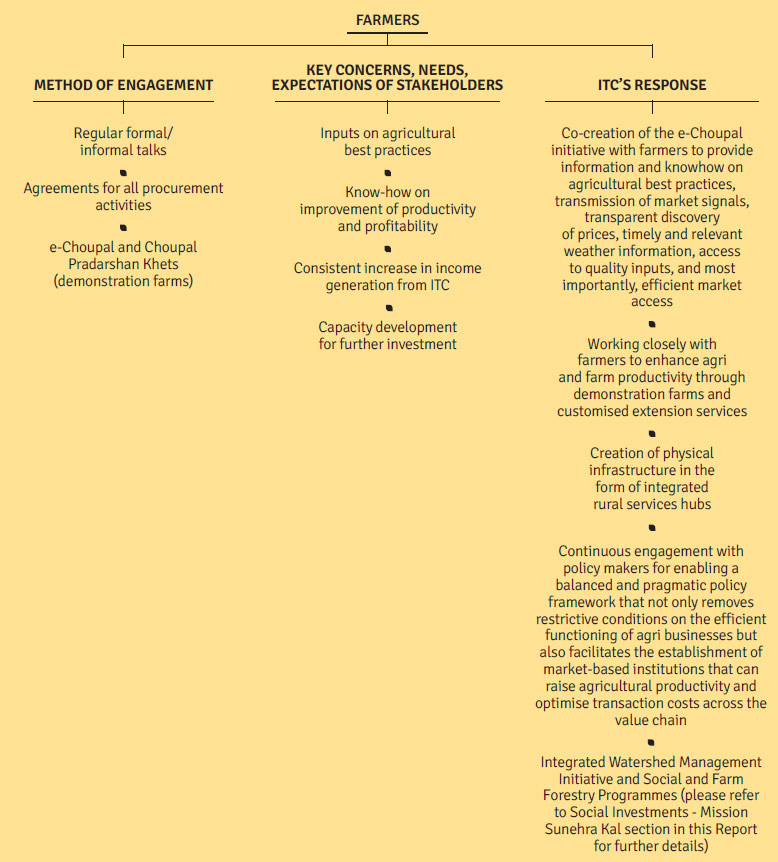

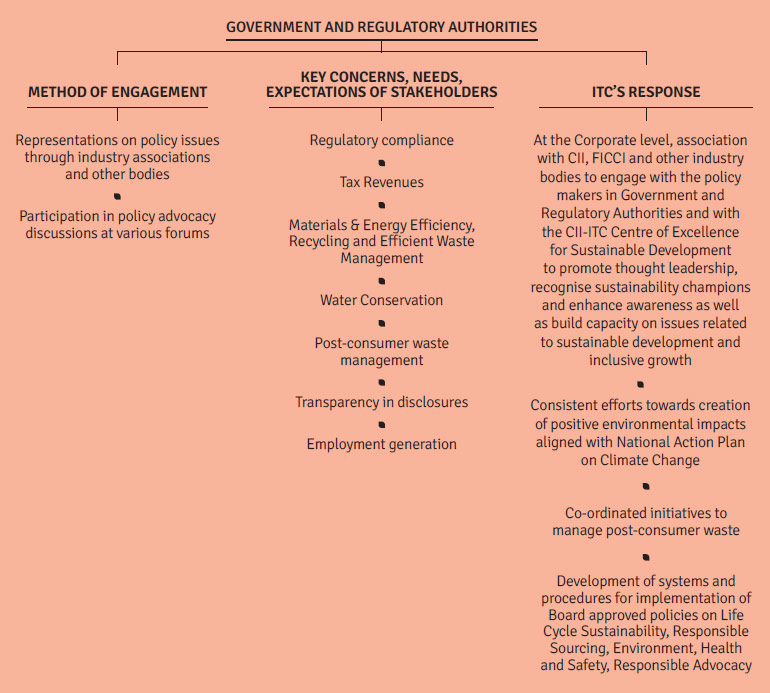

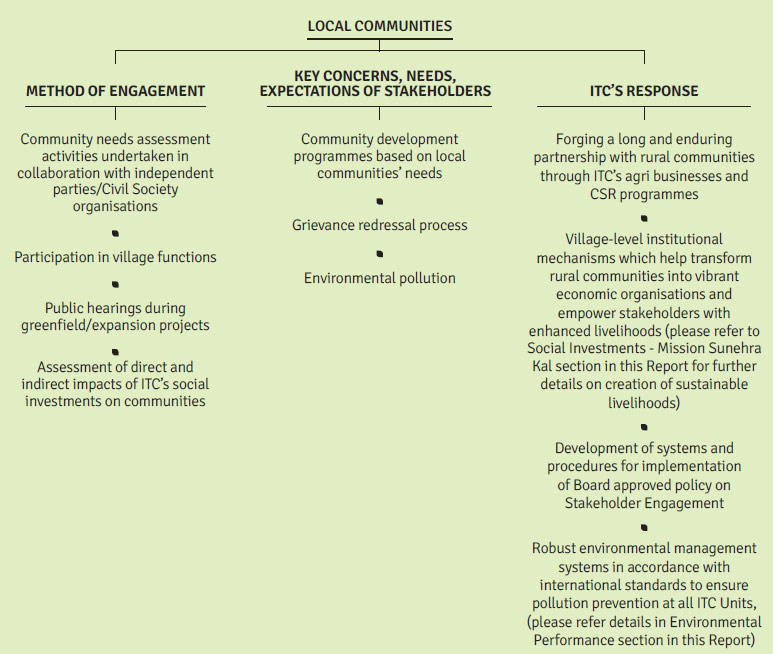

For each of these identified key stakeholders, the context for stakeholder consultation is established through creation of generic awareness about the organisation's activities and immediate future plans through press releases, website, advertisements & other public presentations and social networking. Stakeholder consultation at ITC is a continual process both at the business as well as at the corporate level, depending on the target stakeholder being engaged with. Targeted consultation processes are conducted on a regular basis, giving due weightage to each stakeholder's nature of engagement with the organisation. The consultative process includes the following:

For each of these identified key stakeholders, the context for stakeholder consultation is established through creation of generic awareness about the organisation's activities and immediate future plans through press releases, website, advertisements & other public presentations and social networking. Stakeholder consultation at ITC is a continual process both at the business as well as at the corporate level, depending on the target stakeholder being engaged with. Targeted consultation processes are conducted on a regular basis, giving due weightage to each stakeholder's nature of engagement with the organisation. The consultative process includes the following: